SANTA FE, N.M. (AP) — A court ruling on Friday put an involuntary manslaughter case against Alec Baldwin on track for trial in early July as a judge denied a request to dismiss the case on complaints that key evidence was damaged by the FBI during forensic testing.

Judge Mary Marlowe Sommer sided with prosecutors in rejecting a motion to dismiss the case.

Defense attorneys had argued that the gun in the fatal shooting was heavily damaged during FBI forensic testing before it could be examined for possible modifications or problems that might exonerate the actor-producer.

The ruling removes one of the last hurdles before prosecutors can bring the case to trial with jury selection scheduled for July 9 in Santa Fe.

At trial, attorneys plan to call on witnesses from a court-approved list of more than 60 people. They include film director Joel Souza, who was wounded in the shooting as well as assistant director Dave Halls, who earlier pleaded no contest to negligent use of a deadly weapon, and an array of first responders, investigators, firearms experts and close-range witnesses to the shooting.

Baldwin isn't listed but has the right to testify at his own trial.

During a rehearsal on the set of the Western film “Rust” in 2021, Baldwin pointed a gun at cinematographer Halyna Hutchins when the revolver went off, killing her and injuring director Souza as the bullet became lodged in his shoulder. Baldwin has maintained that he pulled back the gun’s hammer but not the trigger and has pleaded not guilty.

The FBI conducted an accidental discharge test on the gun by striking it from several angles with a rawhide mallet, eventually breaking the gun. Prosecutors plan to present evidence at trial that they say shows the firearm “could not have fired absent a pull of the trigger” and was working properly before the shooting.

Baldwin has twice been charged in Hutchins’ death. Prosecutors dismissed an earlier charge, then refiled it after receiving a new analysis of the revolver that Baldwin pointed at Hutchins.

“Rust” armorer Hannah Gutierrez-Reed is serving an 18 month sentence on a conviction for involuntary manslaughter in the fatal shooting, as she appeals the jury verdict. It's likely the prosecutors will call her to testify at Baldwin's trial, despite her refusal to answer questions at a pretrial interview and instead invoke her constitutional rights against self-incrimination under the Fifth Amendment. A judge refused a request to compel her testimony by providing immunity.

Marlowe Sommer said that destruction of internal components of the firearm “is not highly prejudicial” to a fair trial and that Baldwin's legal team failed to demonstrate bad faith by investigators.

While Baldwin “contends that an unaltered firearm is critical to his case, other evidence concerning the functionality of the firearm on Oct. 21, 2021, weighs against the defendant’s assertions,” the judge wrote.

Sheriff’s investigators initially sent the revolver to the FBI for routine testing, but when an FBI analyst heard Baldwin say in an ABC TV interview that he never pulled the trigger, the agency told local authorities they could conduct an accidental discharge test, though it might damage the gun.

The FBI was told by a team of investigators to go ahead, and tested the revolver by striking it from several angles with a rawhide mallet. One of those strikes fractured the gun’s firing and safety mechanisms.

Defense attorneys say that the “outrageous” decision to move forward with testing may have destroyed exculpatory evidence.

Prosecutors said it was “unfortunate” the gun broke, but it wasn’t destroyed and the parts are still available. They say Baldwin’s attorneys still have the ability to defend their client and question the evidence against him.

In Friday's ruling, the judge said prosecutors will have to fully disclose at trial the destructive nature of the FBI forensic testing on the gun, including what was lost in the process and its relevance in reaching a verdict.

Several hours of testimony about the gun and forensic testing during online hearings in recent days provided a dress rehearsal for the possible trial against Baldwin. Attorneys for Baldwin gave long and probing cross-examinations of the lead detective, an FBI forensic firearm investigator and the prosecution’s independent gun expert, Lucien Haag.

Prosecutors plan to present evidence that they say shows the firearm “could not have fired absent a pull of the trigger” and was working properly before the shooting.

Since the 2021 shooting, the filming of “Rust” resumed but moved to Montana under an agreement with Hutchins’ husband, Matthew Hutchins, which made him an executive producer. The completed movie has not yet been released for public viewing.

FILE - This aerial photo shows the movie set of "Rust," at Bonanza Creek Ranch, Oct. 23, 2021, in Santa Fe, N.M. A court ruling Friday, June 28, 2024, put an involuntary manslaughter case against Alec Baldwin on track for trial in early July as a judge denied a request to dismiss the case on complaints that key evidence was damaged by the FBI during forensic testing. (AP Photo/Jae C. Hong, File)

FILE - Alec Baldwin emcees the Robert F. Kennedy Human Rights Ripple of Hope Award Gala at New York Hilton Midtown on Dec. 9, 2021, in New York. A court ruling Friday, June 28, 2024, put an involuntary manslaughter case against Baldwin on track for trial in early July as a judge denied a request to dismiss the case on complaints that key evidence was damaged by the FBI during forensic testing. (Photo by Evan Agostini/Invision/AP, File)

LONDON--(BUSINESS WIRE)--Jul 1, 2024--

The last year has been challenging for UK households balancing budgets against rising fuel costs, spiralling inflation and wage pressures. Analysis by global analytics software firm FICO of its proprietary UK credit cards data for March 2023 to March 2024 illustrates the impact these pressures have had on credit card usage and debt management.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20240701357732/en/

Overall, consumer spend was up and payments to balance down year-on-year with credit card balances remaining high, having returned to pre-pandemic levels. The 12-month period also saw greater use of credit cards to withdraw cash.

Highlights

FICO Guidance

With customers paying down less of their balances, more customers will fall into the persistent debt category (over a period of 18 months, a customer pays more in interest, fees and charges than they have repaid of the principal). In a Consumer Duty world, FICO recommends that firms are actively identifying these customers at an early stage and reviewing their communications, to encourage higher payments in support of achieving better value from their credit card. This review should be comprehensive and include payment and communications channels which best engage and empower the customer to manage their finances proactively reaching out to customers before they move into each of the persistent debt stages will help to ensure they are on the right product based on their current affordability needs.

With more customers missing payments compared to this time last year, FICO also recommends implementing pre-delinquent strategies and reviewing those already in production to try and reduce the number and amount of balances moving forwards into delinquency. These strategies will support firms in both their attempts to avoid foreseeable customer harm and also carrying potentially avoidable loss provisions, under IFRS 9.

Data and Analysis

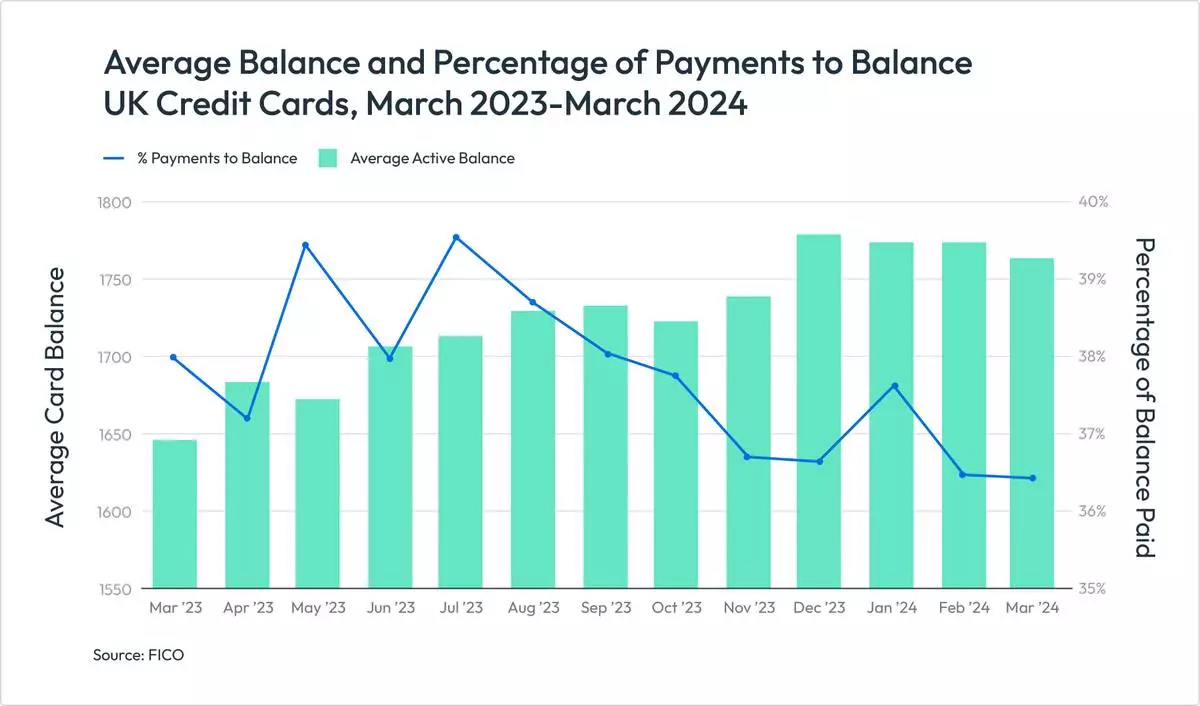

Spending has remained high as payments to balance has trended down

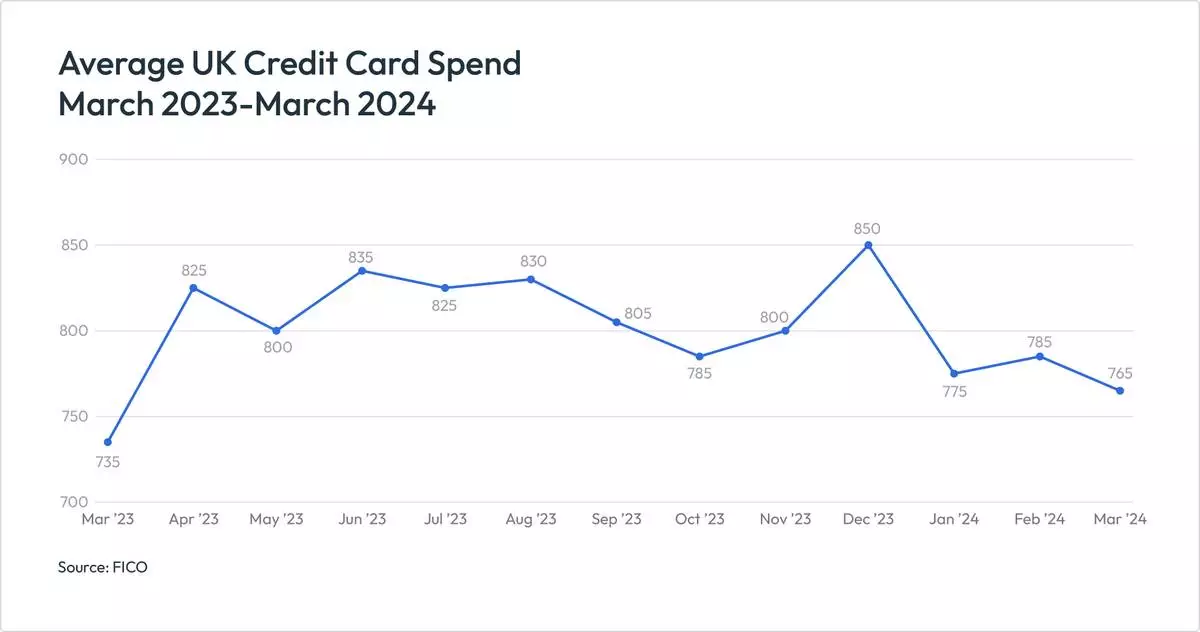

Continued high inflation and higher prices for goods has kept spending high throughout the past 12 months. Seasonal fluctuations have continued as expected, and the level of spending has remained steadfastly higher than 2022-23.

The percentage of payments being made compared to overall balances has been trending down since July 2023 – except for the expected seasonal increase in January 2024. With lockdown and increased savings this reached a high of 42% in May 2022, however it has now fallen to 36.4%. With higher spending and lower repayments, it follows that overall card balances have remained higher than the previous year. Having fallen during the pandemic, balances have now returned to pre-pandemic levels, reaching a record high of £1,780 in December 2023.

FICO advises:

As spending and balances increase and remain high, risk teams should review the number and amount of credit card limits being offered to ensure they increase in line with these higher balances. Customers going over their credit card limit should also be reviewed for potential limit increase offers.

Missed payments for New, Established and Veteran card holders

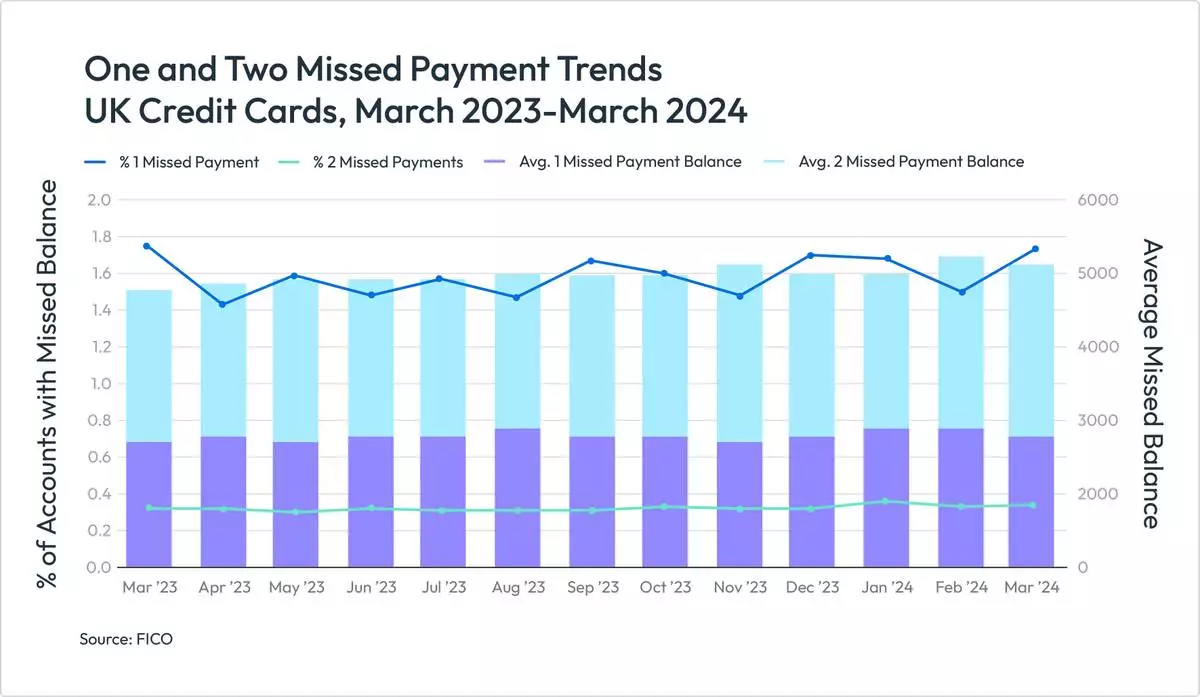

The number of customers missing one, two or three payments has been erratic month-on-month throughout 2023-24. And when comparing year-on-year, the proportion of customers missing payments increased almost every month.

The last 12 months has also seen a change in the behaviour of different segments of cardholders most likely to miss payments.

Before the pandemic, the number of customers missing either one, two or three payments was always higher for the New segment, those who have held the card for less than 12 months. This was expected, as this group of customers had recently taken out cards so were more credit hungry and likely to miss payments. This group also contains first-party fraudsters with no intention of repaying balances.

However, post-pandemic, it is the Established group of customers (those who have held the card for between one and five years) who are now more likely to miss payments. Reasons for this include:

For the Veteran segment, customers who have held their card for more than five years, the increase in missed payments is even more apparent. One, two and three missed payment balances have all increased at a higher rate since December 2023. There were also increases in two missed payment balances between March and August 2023, and again between June and October 2023.

FICO advises: To meet Consumer Duty requirements to proactively reach out before customers become overindebted and affordability issues worsen, risk teams should focus on supporting Established customers who are not managing to pay down their balances. More specialised collections treatment may be appropriate, perhaps moving customers onto a different card that more suits their changing risk profile or reviewing their credit card limit. Supporting customers through challenging times now will boost loyalty and keep them as a long-term customer.

Risk teams should focus on supporting Established customers who are not managing to pay down non-promotional balances, and take proactive action before promotional APRs expire — perhaps move them onto a lower rate, which is also a good incentive to try and keep customers loyal to their bank.

Cash withdrawals on credit cards

In August 2023, UK Finance reported that consumers paying for items in cash had risen for the first time in a decade. This increase in cash usage was also reflected in FICO’s benchmarking figures, which saw a steady increase in the percentage of customers using their credit cards to take out cash between March and September 2023. However, this was still significantly lower than pre-pandemic, when an average 6% of customers used credit cards to take out cash compared to 3.7% in September 2023. The trend for more retailers and hospitality businesses to only accept card payments is likely to be a factor in this shift.

Since September 2023, cash withdrawals have dropped back, following a similar trend as witnessed in the previous year which saw a decrease between September 2022 and February 2023 before increasing over the spring and summer months. However, it is worth noting that when comparing 2023-24 to 2022-23, every month has seen more customers using their cards to take out cash than the same month the previous year.

FICO advises:

Analytical teams should review risk models on an annual basis to ensure they still rank-order risk effectively, especially when models segment customers by cash usage. Risk teams should also consider risk-based cash limit strategies, as well as monitoring the number of cash transactions being accepted, even for underlimit customers.

These card performance figures are part of the data shared with subscribers of the FICO ® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO ® TRIAD ® Customer Manager solution in use by some 80% of UK card issuers. For more information on these trends, contact FICO.

About FICO

FICO (NYSE: FICO) powers decisions that help people and businesses around the world prosper. Founded in 1956, the company is a pioneer in the use of predictive analytics and data science to improve operational decisions. FICO holds more than 200 US and foreign patents on technologies that increase profitability, customer satisfaction and growth for businesses in financial services, insurance, telecommunications, health care, retail and many other industries. Using FICO solutions, businesses in more than 100 countries do everything from protecting 4 billion payment cards from fraud, to improving financial inclusion, to increasing supply chain resiliency. The FICO® Score, used by 90% of top US lenders, is the standard measure of consumer credit risk in the US and other countries, improving risk management, credit access and transparency. Learn more at www.fico.com.

FICO and TRIAD are registered trademarks of Fair Isaac Corporation in the U.S. and other countries.

FICO data shows that the number of UK cardholders missing one, two or three payments has been erratic month-on-month throughout 2023-24. When comparing year-on-year, the proportion of customers missing payments increased almost every month. (Graphic: FICO)

FICO data shows that high inflation and higher prices for goods have kept spending high on UK credit cards throughout the past 12 months. Seasonal fluctuations have continued as expected, and the level of spending has remained steadfastly higher than 2022-23. (Graphic: FICO)

FICO data on UK credit cards shows that the percentage of payments being made compared to overall balances has been trending down since July 2023. (Graphic: FICO)