AUSTIN, Texas (AP) — Two indictments against former Uvalde, Texas, schools police officers are the first charges brought against law enforcement for the botched response that saw hundreds of officers wait more than an hour to confront an 18-year-old gunman who killed 19 fourth-grade students and two teachers at Robb Elementary.

For some Uvalde families, who have spent the last two years demanding police accountability, the indictments brought a mix of relief and frustration. Several wonder why more officers have not been charged for waiting to go into the classroom, where some victims lay dying or begging for assistance, to help bring a quicker end to one of the worst school shootings in U.S. history.

Former Uvalde schools police Chief Pete Arredondo and former Officer Adrian Gonzales were indicted on June 26 by a Uvalde County grand jury on multiple counts of child endangerment and abandonment over their actions and failure to immediately confront the shooter. They were among the first of nearly 400 federal, state and local officers who converged on the school that day.

“I want every single person who was in the hallway charged for failure to protect the most innocent,” said Velma Duran, whose sister Irma Garcia was one of the teachers killed. “My sister put her body in front of those children to protect them, something they could have done. They had the means and the tools to do it. My sister had her body.”

Uvalde County District Attorney Christina Mitchell has not said if any other officers will be charged or if the grand jury's work is done.

Here are some things to know about the criminal investigation into the police response:

The gunman stormed into the school on May 24, 2022 and killed his victims in two classrooms.

More than 370 officers responded but waited more than 70 minutes to confront the shooter, even as he could be heard firing an AR-15-style rifle.

Terrified students inside the classrooms called 911 as agonized parents begged for intervention by officers, some of whom could hear shots being fired while they stood in a hallway. A tactical team of officers eventually went into the classroom and killed the shooter.

Scathing state and federal investigative reports on the police response have catalogued “cascading failures” in training, communication, leadership and technology problems.

The indictment against Arredondo, who was the on-site commander at the shooting, accused the chief of delaying the police response despite hearing shots fired and being notified that injured children were in the classrooms and a teacher had been shot.

Arredondo called for a SWAT team, ordered the initial responding officers to leave the building and attempted to negotiate with the 18-year-old gunman, the indictment said. The grand jury said it considered his actions criminal negligence.

Gonzales was accused of abandoning his training and not confronting the shooter, even after hearing gunshots as he stood in a hallway.

All the charges are state jail felonies that carry up to two years in jail if convicted.

Arredondo said in a 2022 interview with the Texas Tribune that he tried to “eliminate any threats, and protect the students and staff.” Gonzalez's lawyer on Friday called the charges “unprecedented in the state of Texas” and said the officer believes he did not break any laws or school district policy.

The first U.S. law enforcement officer ever tried for allegedly failing to act during an on-campus shooting was a campus sheriff’s deputy in Florida who didn’t go into the classroom building and confront the perpetrator of the 2018 Parkland massacre. The deputy, who was fired, was acquitted of felony neglect last year. A lawsuit by the victims’ families and survivors is pending.

The families are pursing accountability from authorities in other state and federal courts. Several have filed multiple civil lawsuits.

Two days before the two-year anniversary of the shooting, the families of 19 victims filed a $500 million lawsuit against nearly 100 state police officers who were part of the botched response. The lawsuit accuses the troopers of not following their active shooter training and not confronting the shooter. The highest ranking Department of Public Safety official named as a defendant is South Texas Regional Director Victor Escalon.

The same families also reached a $2 million settlement with the city under which city leaders promised higher standards for hiring and training local police.

On May 24, a group of families sued Meta Platforms, which owns Instagram, and the maker of the video game Call of Duty over claims the companies bear responsibility for the weapons used by the teenage gunman.

They also filed another lawsuit against gun maker Daniel Defense, which made the AR-style rifle used by the gunman.

This photo provided by Uvalde County Sheriff's Office shows Pete Arredondo. Arredondo, the former police chief for schools in Uvalde, Texas, was arrested and briefly booked into ail before he was released Thursday, June 27, 2024, on 10 state jail felony counts of abandoning or endangering a child in the May 24, 2022, attack that killed 19 children and two teachers.(Uvalde County Sheriff's Office via AP)

FILE - Uvalde School Police Chief Pete Arredondo, third from left, stands during a news conference outside of the Robb Elementary school on May 26, 2022, in Uvalde, Texas. Arredondo was arrested and briefly booked into the Uvalde County jail before he was released Thursday, June 27, 2024, on 10 state jail felony counts of abandoning or endangering a child in the May 24, 2022, attack that killed 19 children and two teachers. (AP Photo/Dario Lopez-Mills, File)

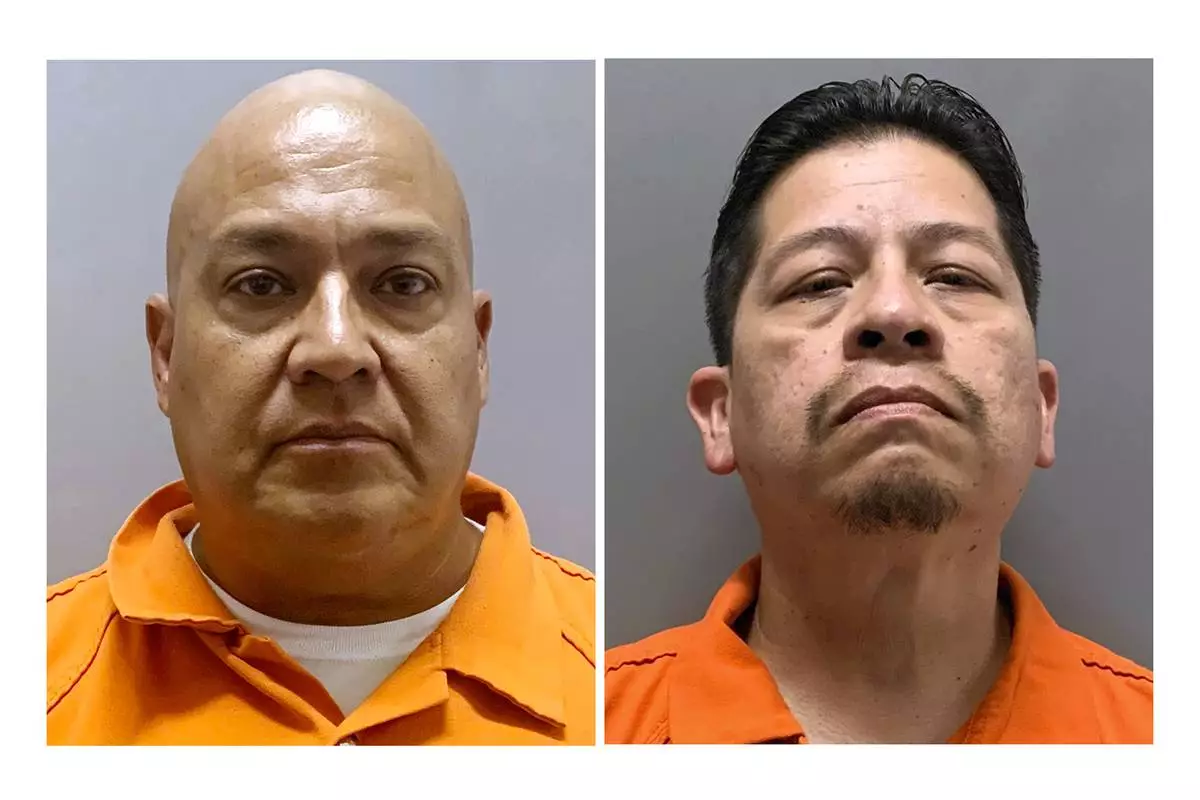

This combo of booking images provided by Uvalde County, Texas, Sheriff's Office, shows Pete Arredondo, left, the former police chief for schools in Uvalde, Texas, and Adrian Gonzales, a former police officer for schools in Uvalde, Texas, Both men were arrested and booked into jail before they were released on charges related to the May 24, 2022, attack that killed 19 children and two teachers at at Robb Elementary. (Uvalde County Sheriff's Office via AP)

LONDON--(BUSINESS WIRE)--Jul 1, 2024--

The last year has been challenging for UK households balancing budgets against rising fuel costs, spiralling inflation and wage pressures. Analysis by global analytics software firm FICO of its proprietary UK credit cards data for March 2023 to March 2024 illustrates the impact these pressures have had on credit card usage and debt management.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20240701357732/en/

Overall, consumer spend was up and payments to balance down year-on-year with credit card balances remaining high, having returned to pre-pandemic levels. The 12-month period also saw greater use of credit cards to withdraw cash.

Highlights

FICO Guidance

With customers paying down less of their balances, more customers will fall into the persistent debt category (over a period of 18 months, a customer pays more in interest, fees and charges than they have repaid of the principal). In a Consumer Duty world, FICO recommends that firms are actively identifying these customers at an early stage and reviewing their communications, to encourage higher payments in support of achieving better value from their credit card. This review should be comprehensive and include payment and communications channels which best engage and empower the customer to manage their finances proactively reaching out to customers before they move into each of the persistent debt stages will help to ensure they are on the right product based on their current affordability needs.

With more customers missing payments compared to this time last year, FICO also recommends implementing pre-delinquent strategies and reviewing those already in production to try and reduce the number and amount of balances moving forwards into delinquency. These strategies will support firms in both their attempts to avoid foreseeable customer harm and also carrying potentially avoidable loss provisions, under IFRS 9.

Data and Analysis

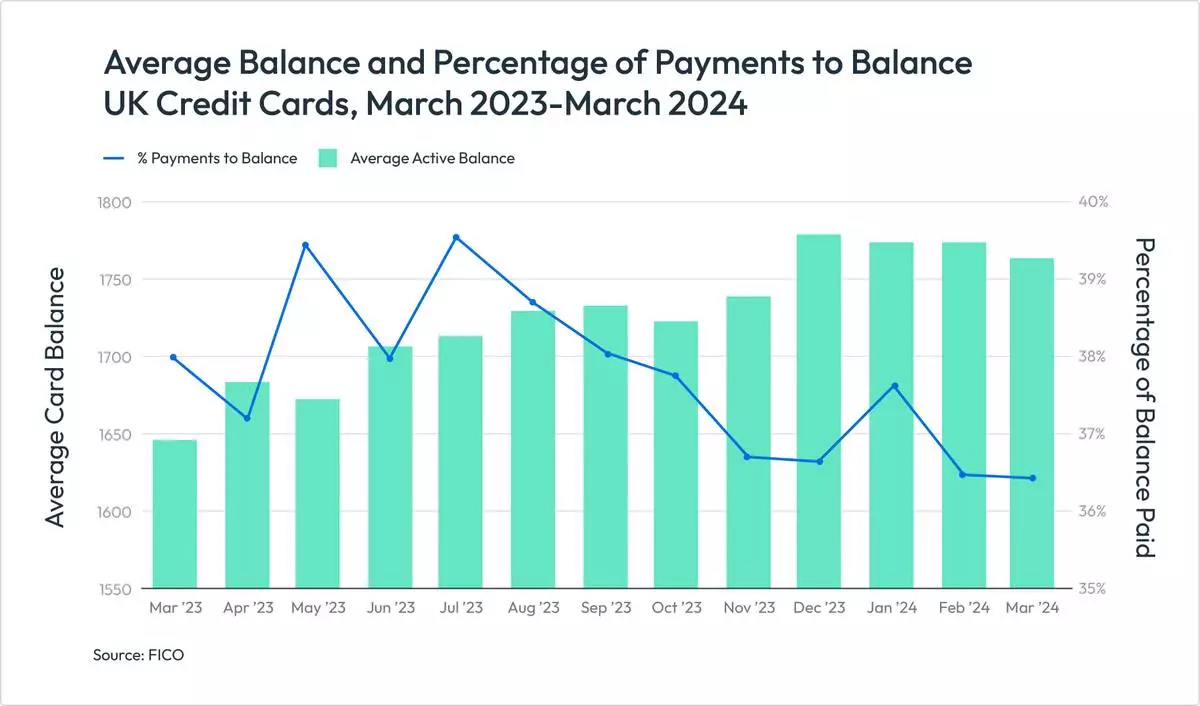

Spending has remained high as payments to balance has trended down

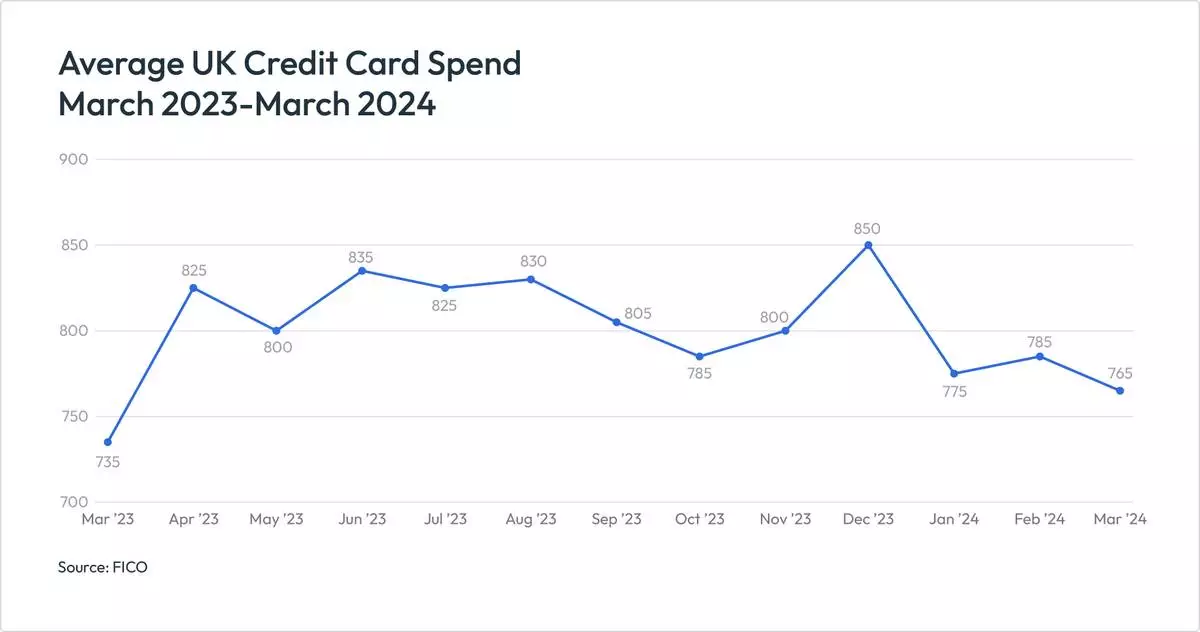

Continued high inflation and higher prices for goods has kept spending high throughout the past 12 months. Seasonal fluctuations have continued as expected, and the level of spending has remained steadfastly higher than 2022-23.

The percentage of payments being made compared to overall balances has been trending down since July 2023 – except for the expected seasonal increase in January 2024. With lockdown and increased savings this reached a high of 42% in May 2022, however it has now fallen to 36.4%. With higher spending and lower repayments, it follows that overall card balances have remained higher than the previous year. Having fallen during the pandemic, balances have now returned to pre-pandemic levels, reaching a record high of £1,780 in December 2023.

FICO advises:

As spending and balances increase and remain high, risk teams should review the number and amount of credit card limits being offered to ensure they increase in line with these higher balances. Customers going over their credit card limit should also be reviewed for potential limit increase offers.

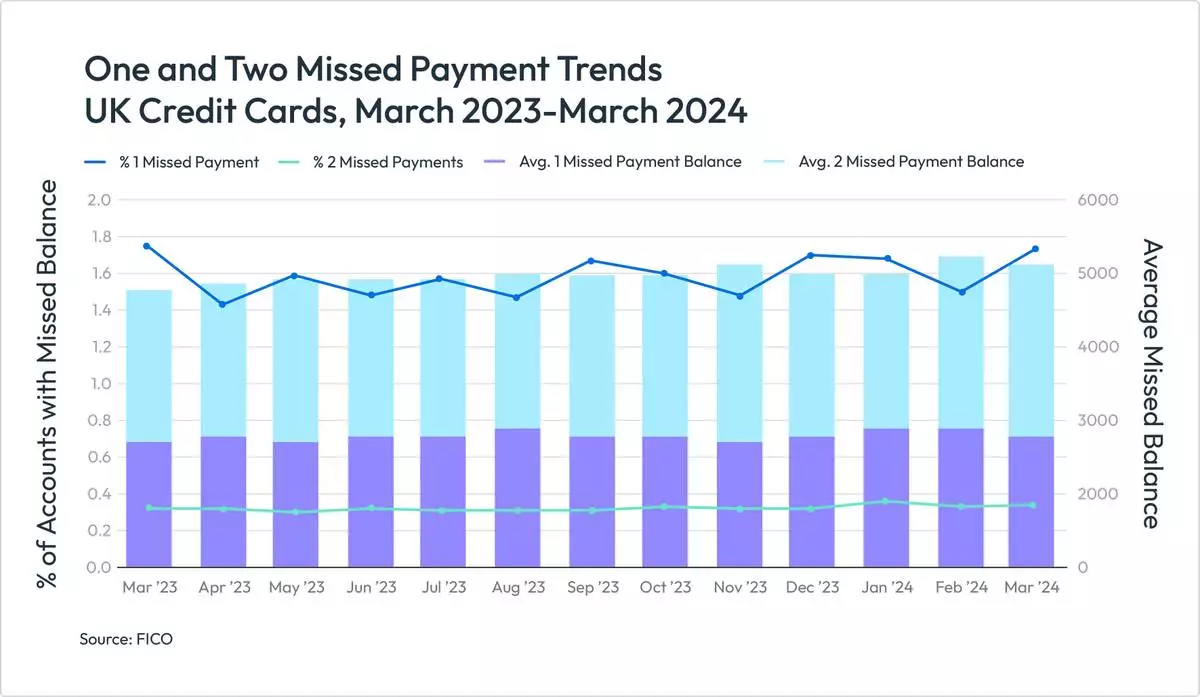

Missed payments for New, Established and Veteran card holders

The number of customers missing one, two or three payments has been erratic month-on-month throughout 2023-24. And when comparing year-on-year, the proportion of customers missing payments increased almost every month.

The last 12 months has also seen a change in the behaviour of different segments of cardholders most likely to miss payments.

Before the pandemic, the number of customers missing either one, two or three payments was always higher for the New segment, those who have held the card for less than 12 months. This was expected, as this group of customers had recently taken out cards so were more credit hungry and likely to miss payments. This group also contains first-party fraudsters with no intention of repaying balances.

However, post-pandemic, it is the Established group of customers (those who have held the card for between one and five years) who are now more likely to miss payments. Reasons for this include:

For the Veteran segment, customers who have held their card for more than five years, the increase in missed payments is even more apparent. One, two and three missed payment balances have all increased at a higher rate since December 2023. There were also increases in two missed payment balances between March and August 2023, and again between June and October 2023.

FICO advises: To meet Consumer Duty requirements to proactively reach out before customers become overindebted and affordability issues worsen, risk teams should focus on supporting Established customers who are not managing to pay down their balances. More specialised collections treatment may be appropriate, perhaps moving customers onto a different card that more suits their changing risk profile or reviewing their credit card limit. Supporting customers through challenging times now will boost loyalty and keep them as a long-term customer.

Risk teams should focus on supporting Established customers who are not managing to pay down non-promotional balances, and take proactive action before promotional APRs expire — perhaps move them onto a lower rate, which is also a good incentive to try and keep customers loyal to their bank.

Cash withdrawals on credit cards

In August 2023, UK Finance reported that consumers paying for items in cash had risen for the first time in a decade. This increase in cash usage was also reflected in FICO’s benchmarking figures, which saw a steady increase in the percentage of customers using their credit cards to take out cash between March and September 2023. However, this was still significantly lower than pre-pandemic, when an average 6% of customers used credit cards to take out cash compared to 3.7% in September 2023. The trend for more retailers and hospitality businesses to only accept card payments is likely to be a factor in this shift.

Since September 2023, cash withdrawals have dropped back, following a similar trend as witnessed in the previous year which saw a decrease between September 2022 and February 2023 before increasing over the spring and summer months. However, it is worth noting that when comparing 2023-24 to 2022-23, every month has seen more customers using their cards to take out cash than the same month the previous year.

FICO advises:

Analytical teams should review risk models on an annual basis to ensure they still rank-order risk effectively, especially when models segment customers by cash usage. Risk teams should also consider risk-based cash limit strategies, as well as monitoring the number of cash transactions being accepted, even for underlimit customers.

These card performance figures are part of the data shared with subscribers of the FICO ® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO ® TRIAD ® Customer Manager solution in use by some 80% of UK card issuers. For more information on these trends, contact FICO.

About FICO

FICO (NYSE: FICO) powers decisions that help people and businesses around the world prosper. Founded in 1956, the company is a pioneer in the use of predictive analytics and data science to improve operational decisions. FICO holds more than 200 US and foreign patents on technologies that increase profitability, customer satisfaction and growth for businesses in financial services, insurance, telecommunications, health care, retail and many other industries. Using FICO solutions, businesses in more than 100 countries do everything from protecting 4 billion payment cards from fraud, to improving financial inclusion, to increasing supply chain resiliency. The FICO® Score, used by 90% of top US lenders, is the standard measure of consumer credit risk in the US and other countries, improving risk management, credit access and transparency. Learn more at www.fico.com.

FICO and TRIAD are registered trademarks of Fair Isaac Corporation in the U.S. and other countries.

FICO data shows that the number of UK cardholders missing one, two or three payments has been erratic month-on-month throughout 2023-24. When comparing year-on-year, the proportion of customers missing payments increased almost every month. (Graphic: FICO)

FICO data shows that high inflation and higher prices for goods have kept spending high on UK credit cards throughout the past 12 months. Seasonal fluctuations have continued as expected, and the level of spending has remained steadfastly higher than 2022-23. (Graphic: FICO)

FICO data on UK credit cards shows that the percentage of payments being made compared to overall balances has been trending down since July 2023. (Graphic: FICO)