China's central bank on Thursday unveiled a new swap facility to bolster the growth of the country's capital markets, a strategic move which aims to ensure the steady development of China's financial landscape in the long term, according to industry experts.

People's Bank of China announced that it has decided to set up Securities, Funds and Insurance companies Swap Facility (SFISF), with the initial scale of 500 billion yuan (about 71 billion U.S. dollars).

The SFISF will allow eligible securities, funds and insurance companies to use their assets including bonds, stock ETFs and holdings in constituents of the CSI 300 Index as collateral in exchange for highly liquid assets such as treasury bonds and central bank bills, said a statement.

Industry experts anticipate the newly-launched swap facility will inject significant additional funds into the capital market and reduce risks for non-bank entities amid market downturns.

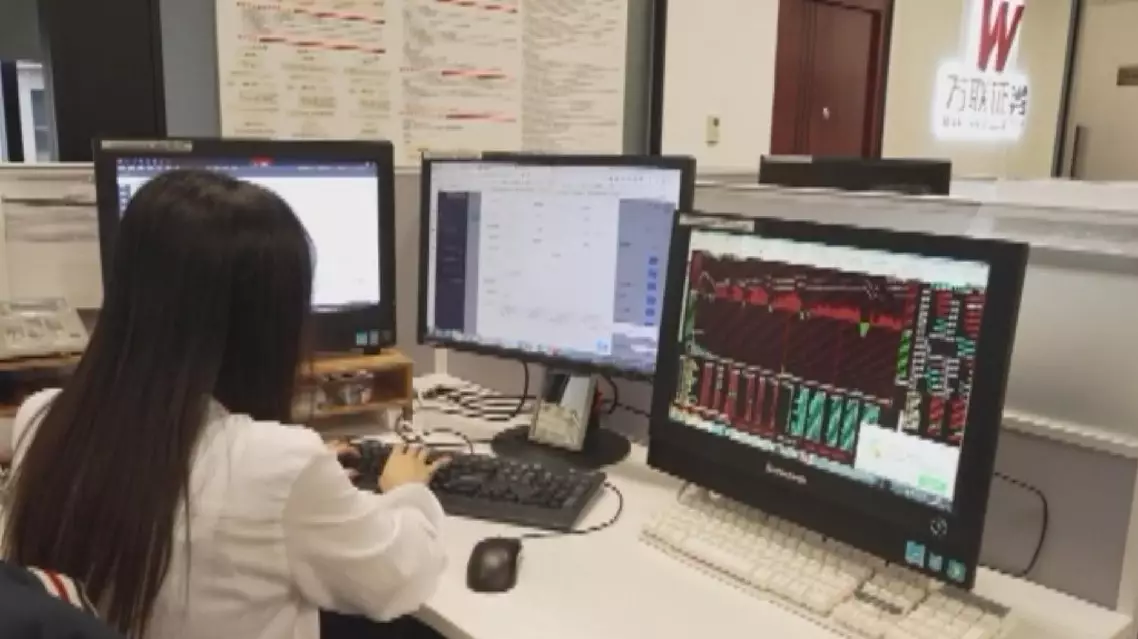

"This greatly enhances the stock holding capacity of securities, funds, and insurance companies, and their ability to acquire funds. Especially when the market is undervalued, these non-bank entities can easily tap into market liquidity using this tool to strengthen their investments in quality assets so as to ensure market stability," said Xu Fei, an analyst of Wanlian Securities, a state-owned securities company.

Sources close to the central bank revealed that the swap facility has a maturity period of up to one year, with provisions for extension upon maturity.

Industry experts further noted the new monetary policy tool applies a "bonds-for-bonds" principle, which does not expand the scale of the base currency, and is not engaged in quantitative easing.

Furthermore, the swap facility enables non-bank entities to exchange less liquid assets for government bonds or central bank bills, making it easier for repurchase or financing sales in the market.

"The swap facility operates on a 'bonds-for-bonds' model, meaning the central bank does not directly inject funds, thereby avoiding an increase in base currency issuance and quantitative easing. While not involving base currency injections, experiences from the global financial crisis underscores the pivotal role of similar facilities, such as the Federal Reserve's Term Securities Lending Facility (TSLF), in swiftly stabilizing financial markets," said Wen Bin, chief economist at Minsheng Bank.

Starting Thursday, applications from eligible securities, funds and insurance companies will be accepted.

China's new 500 billion yuan swap facility to bolster capital market: experts