SAN FRANCISCO--(BUSINESS WIRE)--Mar 14, 2025--

Leading measurement and analytics company Adjust today released its annual Gaming App Insights 2025 report, showing a resilient gaming industry on the other side of a challenging 2023. Global gaming app installs increased by 4% YoY in 2024, but sessions dipped slightly (-0.6%) – making 2025 a moment to maintain momentum while improving core metrics like retention and user stickiness.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20250314915427/en/

“After a period of market volatility, mobile gaming is back on a growth trajectory,” noted Tiahn Wetzler, Director of Content and Insights at Adjust. "As mobile-first adoption accelerates in regions like LATAM and MENA, game developers and marketers that prioritize long-term player relationships over short-term acquisition will reap the rewards.”

Emerging markets leading mobile gaming growth

Adjust found that MENA (+10%) and LATAM (+8%) led global gaming app install growth in 2024, while sessions increased 7% and 5%, respectively. In contrast, North America saw the steepest decline, with installs down 11% and sessions dropping 14%, signaling user engagement challenges.

Elsewhere, APAC posted mixed results: Installs grew 4% but sessions declined 3%, indicating retention challenges. Europe experienced a drop in installs (-1%) and sessions (-6%), reflecting possible issues with user engagement.

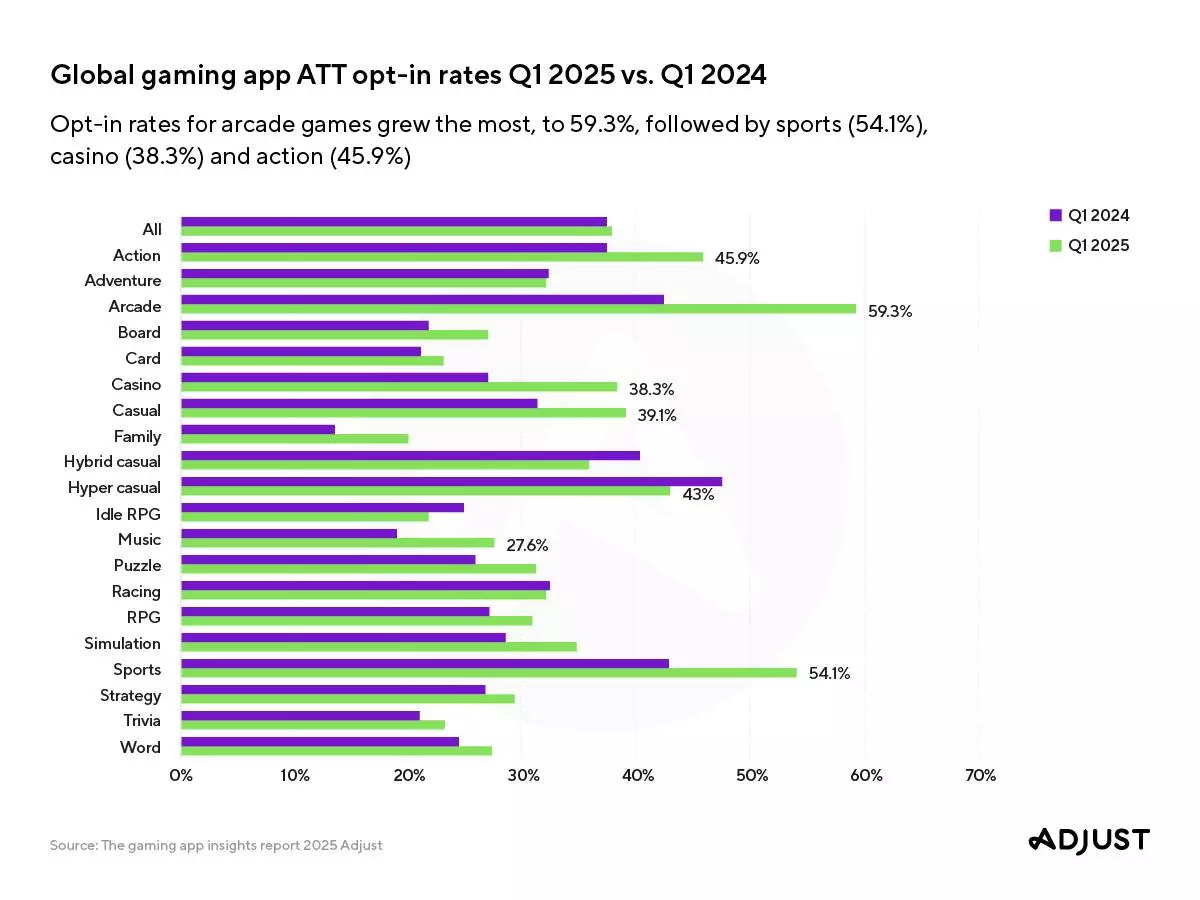

ATT opt-in rates seeing incremental growth globally

Gaming App Tracking Transparency (ATT) opt-in rates increased slightly in Q1 of 2025 to 37.9% from 37.5% in the same quarter of 2024. Arcade games saw the most significant growth, with opt-ins jumping from 42.4% to 59.3%. Sports (54.1%), casino (38.3%) and action (45.9%) games also saw gains, while hyper casuals experienced a slight drop. Regionally, MENA’s markets remained strong, with opt-in rates hovering around 50%, and U.S. rates held steady at approximately 32%.

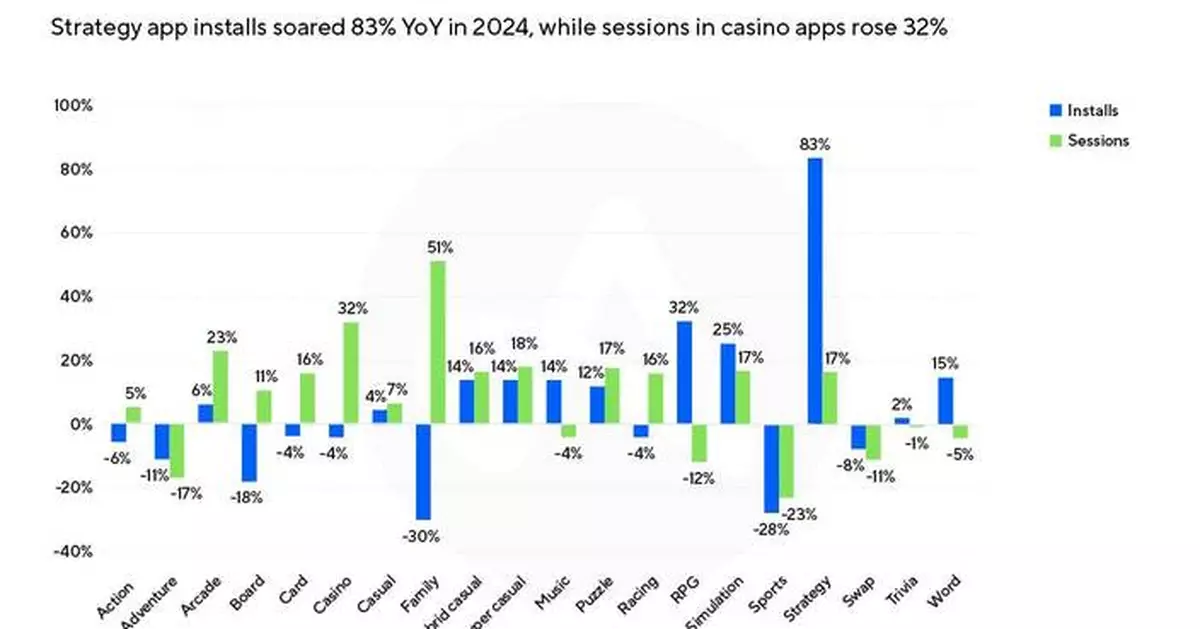

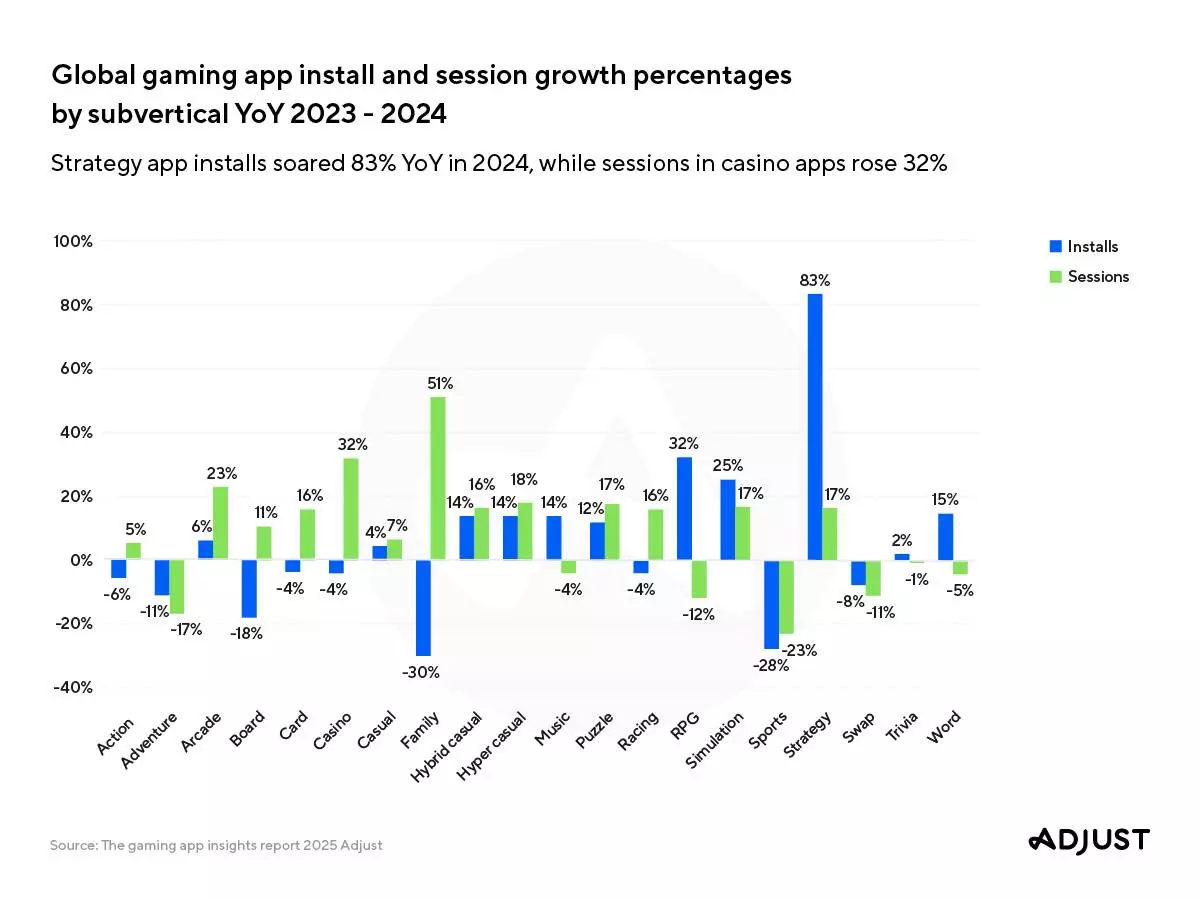

Gaming subvertical install and session growth patterns

Adjust’s data shows hyper casual games retained the highest global installs share (27%) in 2024, but contributed only 11% of sessions, underscoring high churn rates. On the other hand, action games, despite representing only 10% of installs, generated 21% of sessions, demonstrating strong retention and ongoing user engagement. Gamers spent the most time playing action games, with an average session length of 45.15 minutes.

Notably, strategy apps had the highest YoY install growth at 83%, while casino (+32%) and arcade (+23%) apps saw the strongest session growth, showing high user engagement.

Key overall shifts Adjust observes in the mobile gaming industry in 2025 include:

For additional findings and industry best practices, download the full report here.

About Adjust

Adjust, an AppLovin (NASDAQ: APP) company, is trusted by marketers around the world to measure and grow their apps across platforms, from mobile to CTV and beyond. Adjust works with companies at every stage of the app marketing journey, from fast-growing digital brands to brick-and-mortar companies launching their first apps. Adjust's powerful measurement and analytics provide visibility, insights and essential tools that drive better results.

Idle RPGs declined from 24.9% to 21.8%, and hyper casual games dropped from 47.5% to 43%. Getting opt-in messaging right is the key to building and maintaining a high rate.

While hyper casual, hybrid casual, puzzle and simulation games all continued to expand, RPG told a different story: Despite a 32% spike in installs, sessions dropped 12%, pointing to retention challenges.

Wall Street followed global markets lower early Monday ahead of the Trump administration's latest tariff rollout later this week.

Futures for the S&P 500 sank 1.2%, while futures for the Dow Jones Industrial Average dropped 0.7%. Futures for the Nasdaq, where many of the biggest U.S. technology companies trade, tumbled 1.6%.

Tesla's woes continued as Elon Musk's electric car company slid 6.1%. Tesla is down 42% since Trump took office Jan. 20, with losses driven in part by the public perception of Musk's oversight of the new Department of Government Efficiency that’s slashing government spending.

Tesla sales in Europe and the U.S. have fallen, partly due to Musk’s political shift to the right. Protestors have targeted the automaker’s showrooms, vehicle lots and charging stations, with some resorting to vandalism, including burning privately owned vehicles.

Apple shares were down less than 1% after France’s antitrust watchdog fined the tech giant $162 million over the rollout of a privacy feature resulted in abuse of competition law.

Shares of the mortgage company Rocket fell 3.5% after it announced that it is buying competitor Mr. Cooper in an all-stock deal valued at $9.4 billion. Mr. Cooper shares soared more than 26%. The deals comes just weeks after Rocket acquired real estate listing company Redfin.

The price of gold hit a record high before inching back down to $3,149 an ounce. Investors continue to pull out of equities in search of traditional safe havens like gold.

Markets worldwide have been anxious over a potentially toxic mix of worsening inflation and a slowing U.S. economy because households are afraid to spend due to the deepening trade war, escalated U.S. by President Donald Trump.

Trump has dubbed Wednesday “Liberation Day,” when he will roll out tariffs tailored to each of the United States’ trading partners that he promises will free the the country from foreign goods.

The details of Trump’s next round of import taxes are still sketchy. Most economic analyses say average U.S. families would have to absorb the cost of his tariffs in the form of higher prices and lower incomes. That has contributed to significant decline in U.S. consumer confidence this year, which has alarmed investors.

On Friday, the S&P 500 fell 2% for one of its worst days in the last two years. It was its fifth losing week in the last six, helping to drive the index down 5% this year. The Dow sank 1.7% and the Nasdaq composite fell 2.7% and is down more than 10% in 2025.

Many of the countries that run trade surpluses with the U.S. and depend heavily on export manufacturing are in Asia, Stephen Innes of SPI Asset Management said in a commentary.

“Asia is ground zero. Of the 21 countries under USTR (U.S. Trade Representative) scrutiny, nine are in Asia,” Innes noted.

Tokyo’s benchmark fell 4.1% to 35,617.56, while the Hang Seng in Hong Kong lost 1.3% to 23,119.58.

The Shanghai Composite index declined 0.5% to 3,335.75.

In South Korea, the Kospi fell 3% to 2,481.12, while Australia’s S&P/ASX 200 sank 1.7%, closing at 7,843.40.

Taiwan’s Taiex lost 4.2%.

European markets opened lower. Britain's FTSE 100 slid 1.4%, while France's CAC 40 and Germany's DAX each fell 2%.

Thailand’s SET lost 1.3% after a powerful earthquake centered in Myanmar rattled the region, causing widespread destruction in the country, also known as Burma, and less damage in places like Bangkok.

Shares in Italian Thai Development, developer of a partially built 30-story high-rise office building under construction that collapsed, tumbled 27%. Thai officials said they are investigating the cause of the disaster, which left dozens of construction workers missing.

A currency trader walks by the screens showing the foreign exchange rate between U.S. dollar and South Korean won, left, and the Korean Securities Dealers Automated Quotations (KOSDAQ) at a foreign exchange dealing room in Seoul, South Korea, Monday, March 31, 2025. (AP Photo/Lee Jin-man)

The screens showing the Korea Composite Stock Price Index (KOSPI), left, the foreign exchange rate between U.S. dollar and South Korean won and the Korean Securities Dealers Automated Quotations (KOSDAQ) are seen at a foreign exchange dealing room in Seoul, South Korea, Monday, March 31, 2025. (AP Photo/Lee Jin-man)

An electronic stock board shows that Nikkei stock average dropped over 1,500 Japanese yen in Tokyo Monday, March 31, 2025. (Kyodo News via AP)

A currency trader works under an electronic stock board at a foreign currency trading firm in Tokyo Monday, March 31, 2025. (Kyodo News via AP)